A python package for time series forecasting with scikit-learn estimators.

tspiral is not a library that works as a wrapper for other tools and methods for time series forecasting. tspiral directly provides scikit-learn estimators for time series forecasting. It leverages the benefit of using scikit-learn syntax and components to easily access the open source ecosystem built on top of the scikit-learn community. It easily maps a complex time series forecasting problems into a tabular supervised regression task, solving it with a standard approach.

tspiral provides 4 optimized forecasting techniques:

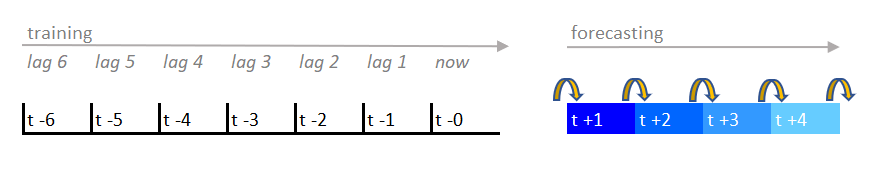

- Recursive Forecasting

Lagged target features are combined with exogenous regressors (if provided) and lagged exogenous features (if specified). A scikit-learn compatible regressor is fitted on the whole merged data. The fitted estimator is called iteratively to predict multiple steps ahead.

Which in a compact way we can summarize in:

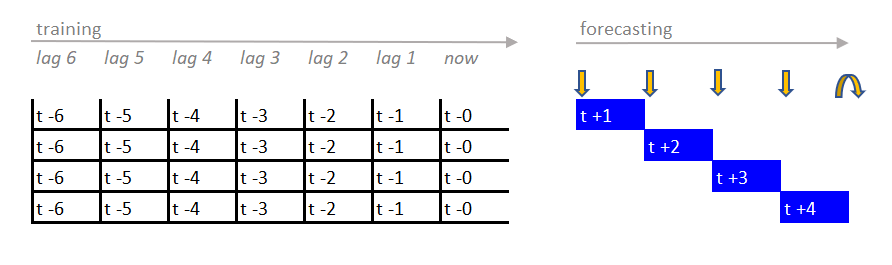

- Direct Forecasting

A scikit-learn compatible regressor is fitted on the lagged data for each time step to forecast.

Which in a compact way we can summarize in:

It's also possible to mix recursive and direct forecasting by predicting directly some future horizons while using recursive on the remaining.

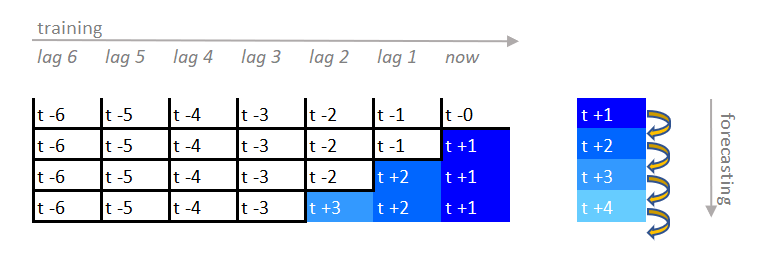

- Stacking Forecasting

Multiple recursive time series forecasters are fitted and combined on the final portion of the training data with a meta-learner.

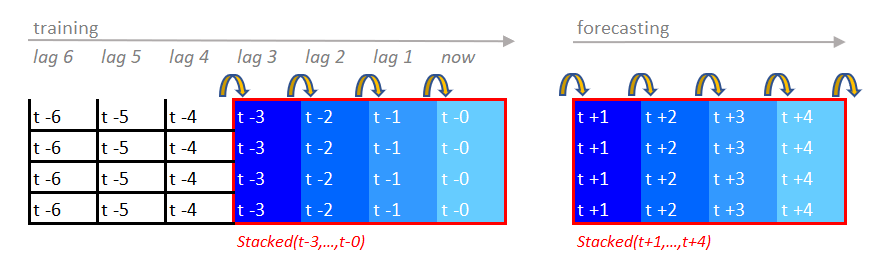

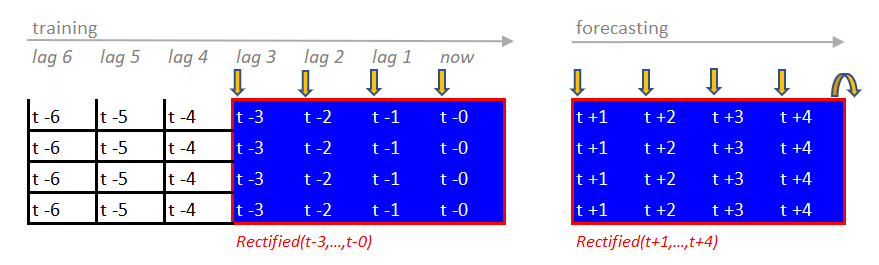

- Rectified Forecasting

Multiple direct time series forecasters are fitted and combined on the final portion of the training data with a meta-learner.

GLOBAL and MULTIVARIATE time series forecasting are natively supported for all the forecasting methods available. For GLOBAL forecasting, use the groups parameter to specify the column of the input data that contains the group identifiers. For MULTIVARIATE forecasting, pass a target with multiple columns when calling fit.

pip install --upgrade tspiralThe module depends only on NumPy, Pandas, and Scikit-Learn (>=0.24.2). Python 3.6 or above is supported.

- How to Improve Recursive Time Series Forecasting

- Time Series Forecasting with Feature Selection: Why you may need it

- Forecast Time Series with Missing Values: Beyond Linear Interpolation

- Time Series Forecasting with Conformal Prediction Intervals: Scikit-Learn is All you Need

- Hitting Time Forecasting: The Other Way for Time Series Probabilistic Forecasting

- Hitchhiker’s Guide to MLOps for Time Series Forecasting with Sklearn

- Recursive Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from tspiral.forecasting import ForecastingCascade

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingCascade(

Ridge(),

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)- Direct Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from tspiral.forecasting import ForecastingChain

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingChain(

Ridge(),

n_estimators=24,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)- Stacking Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.tree import DecisionTreeRegressor

from tspiral.forecasting import ForecastingStacked

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingStacked(

[Ridge(), DecisionTreeRegressor()],

test_size=24*3,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)- Rectified Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.tree import DecisionTreeRegressor

from tspiral.forecasting import ForecastingRectified

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingRectified(

[Ridge(), DecisionTreeRegressor()],

n_estimators=24*3,

test_size=24*3,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)More examples in the notebooks folder.